Personal Finance: Building Wealth Through Digital Budgeting

![]()

Personal Finance: Building Wealth Through Digital Budgeting

These days, tech and finance seem to be more intermingled than at any other point in human history. Surging valuations in the biggest tech companies (like Apple, Amazon, and Facebook) show that the dominant trends in the market will continue to be tied to the world of technology. But it is up to consumers to take action and to make real progress in controlling monthly finances.

But even with all of the incredible new personal finance tools that are currently available, most Americans still have a hard time creating and managing a workable household budget. To be fair, recent studies have shown that 84% of Americans will say that they keep a monthly budget – and that is much higher than the reported figure of 60% seen in 2012.

Detailing Expenses

Unfortunately, 20% of this year’s numbers respondents say that they only keep a mental record of their household budgeting expenditures. Mental accounting has always been notoriously unreliable, as it leaves consumers vulnerable to mistakes or illogical spending rationalizations.

Ultimately, this suggests most Americans show a lack of basic knowledge about some critical issues. In everyday practice, this is exemplified by the fact that less than 40% of Americans have $500 or $1,000 saved in the case of a major emergency (i.e. a significant medical bill, major car repair, or other expense).

If a major expense were to arise, a substantial 25% of these consumers say that they would cut back on spending in order to make up for the budgeting differences. This is not entirely a terrible idea on its own, but it does suggest that a higher level of planning will need to be seen in the America consumer going forward.

What is more troublesome is that 16% say they would request a loan from friends or another family member while another 12% say they would add the charges to a credit card. The best remedy for these types of situations is to have a proper planning strategy for all personal finances. Personal finance apps and budget tracking tools will allow you to monitor spending habits in a more objective way. Knowing where your money goes can help in monitoring finances over the long-term.

Create A Financial Plan

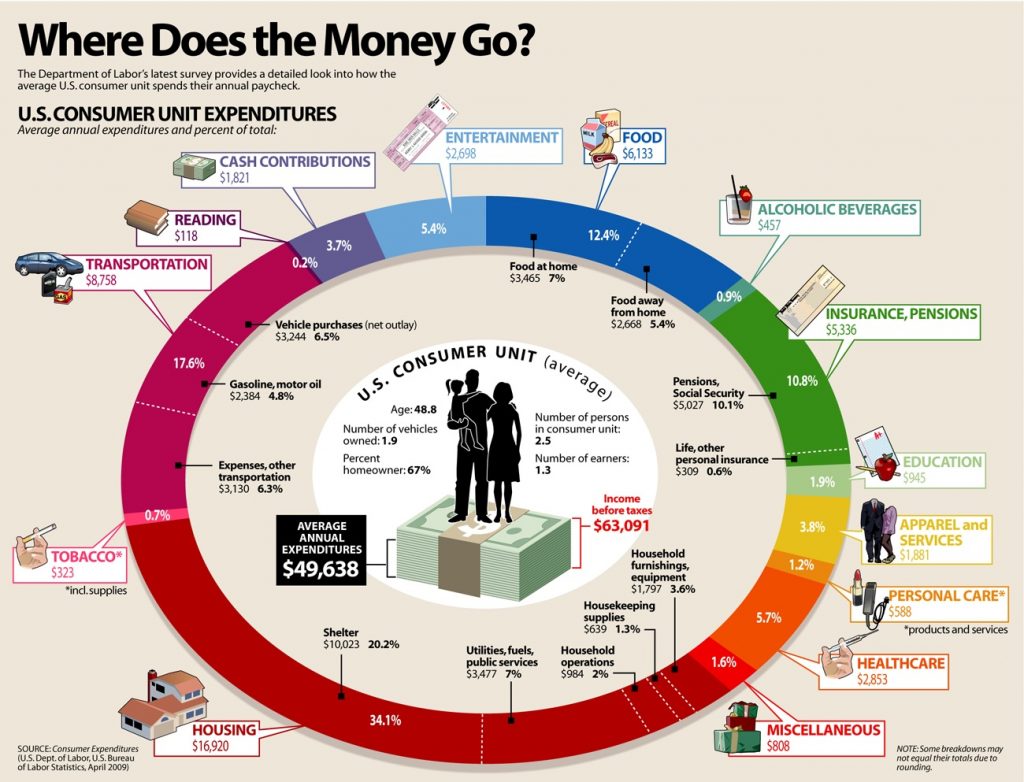

The first part of the process is to identify where exactly household money is going each month. What tends to be most important is the list of regular expenses that are incurred each month. For example, monthly food costs tend to be more regular and consistent than entertainment costs (which can vary more widely).

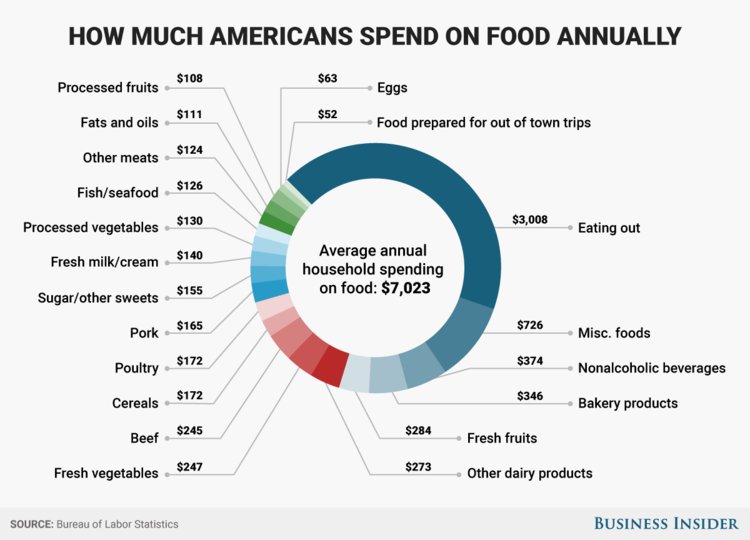

Each list on this chart essentially creates its own internal list that will also need to be budgeted appropriately. Here is an example of the average costs American see each year in their budgeted food costs:

To be sure, this is a lot of information to track. Luckily, there are some amazing tools and strategies available to align your income with your budgeting practices in order to meet your financial goals.

Using a Budgeting App

Personal budget software apps can take the challenge (and boredom) out of the equation when budgeting household expenses for the month. The apps can help consumers find a budgeting strategy that works with a spending plan to meet the needs of households and families. Personal budget software apps come with some pretty handy extra features which can be adjusted depending on your individual needs.

In the end, the goal of personal finance is to build wealth through time. This can be achieved through proper money management techniques and digital budgeting that allows for many of the pitfalls and intricacies that can come at unexpected times. Knowledge and research offer the best ways of preparing for these events, and personal budgeting apps can take out most of the guesswork during this process.