Home Loans: Ways of Financing the American Dream

The housing market in the US continues to move ahead in its recovery and we are seeing more and more consumers looking to make real estate purchases. When you are looking to finance the American Dream, there are many options available to you.

Purchasing a home gives a huge sense of accomplishment – however, not without the frustration and anxiety that is often experienced. This is why it is absolutely essential that potential homebuyers familiarize themselves with the various lending options that are currently available.

Understanding Home Loans

In simple terms, a “mortgage” or “home loan” refers to money that can be borrowed from a bank, credit union, or any other financial institution to put toward the purchase of a new home.

The three basic components of a home loan are:

- Size: The amount of loan money needed is dependent on the price of the house and the borrower’s credit eligibility.

- Length: The amount of time needed to repay the loan, also known as the “loan term.”

- Interest Rate: The interest charged by the lender for the granting access to the loan.

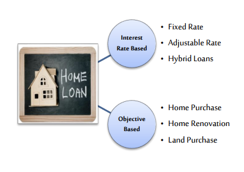

Types of Home Loans

Home loans can be classified into three broad categories:

- INTEREST BASED LOANS:

- Fixed Rate Loans: Interest rates do not fluctuate during the term of the loan. The borrower knows in advance the repayment amounts that will be required during the entire period of the loan. This is helpful for individuals who have a predefined income schedules or are near retirement.

- Adjustable Rate Home Loans: In these loans, the rate of interest varies according to market rates seen during the loan term. The monthly payments in these types of loans vary and they may increase and decrease if the market/index rate fluctuates.

- Hybrid Loans: These are loans which combine the two types of loans above. These loans start with a fixed rate that changes over a period of time to an adjustable rate schedule, in many cases giving flexibility to the borrower.

- OBJECTIVE BASED LOANS:

- Home Purchase Loans: These are loans that are obtained to purchase a new residential property from the current owners.

- Home Renovation Loans: These are loans undertaken to refurbish, extend, or renovate an existing house or a property.

- Land Purchase Loans: These are loans taken when a borrower wants to purchase a plot of land to construct a house, recreational property, or commercial property.

Apart from the above broad categories, the following are some types of loans which are commonly available in the US:

- Government Loans: Loans backed by the Federal Housing Association (FHA), or veterans loans which are backed by the Department of Veteran Affairs.

- Conforming or Non-Conforming Loans: Loans measured against the guidelines prescribed by Fannie Mae and Freddie Mac.

- USDA Rural Housing Loans: Zero down payment loans which can be used only in designated areas and towns.

The home lending market is broadly diverse in terms of the loan products that are currently offered by various banks and finance companies. This is why borrowers must study and compare these different products in order to make an informed decision with their property investments.

Planning and Budgeting a Home Loan

Planning for a home loan is like preparing for a long journey. It takes time, insight, and the right choices. Hence, a prospective borrower must become familiar with the entire loan process to start budgeting income accordingly. This is essential in order for borrowers to know which loan type is most appropriate for the individual situation.

The following diagram helps us to understand the various aspects that are necessary while planning for a home loan:

Understanding the Facts

Borrowers will likely come across some key terms that will be used during the entire loan procedure. Here are some important examples that should become familiar:

- EMI (Equated Monthly Installments): refers to the total amount that the borrower will pay every month to repay the loan. This amount is a combination of the loan amount (principal) and the rate of interest.

- Margin: While constructing a home loan, the bank might pay 80% or 90% of the total amount, while the rest must be paid by the borrower. This amount is known as margin or down payment.

- Eligibility and Credit Appraisal: Before sanctioning the loan, the lender will look into various factors like loans currently serviced, savings, income, age, job qualifications, etc. This is done to determine the credit eligibility of the borrower.

- Property Pre-Approval: The home loan company will examine all the approvals and legal documents of the property along with the track record of the builder.

- Offer Letter/Loan Sanction Letter: This is a letter that is provided to the borrower informing the approved eligibility and this gives a go-ahead to begin the procedure for further formalities (including disbursements).

Qualifying for a Home Loan

A person’s qualification for a home loan is based on the debt-to-income ratio, which is the amount of debt compared to available income. A rate of 43% is considered acceptable for a qualified mortgage.

The following formula is used for calculating the ratio:

![]()

Home Loan Affordability

While applying for a home loan, the lender will calculate the borrower’s eligibility/affordability by taking into account the level of income, down payment and monthly debts.

Individuals can estimate their eligibility by using online calculators on many bank websites.

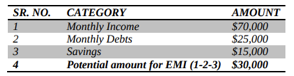

The following example explains the basic calculation of home loan affordability. For someone that wants to take a home loan with a term of 20 years and an interest rate of 10.5%:

By doing a reverse-calculation on the following formula, the affordability amount (Principal) can be calculated:

![]()

Taking EMI as $30,000, the affordable loan amount (P) would come to approximately $3,004,868.

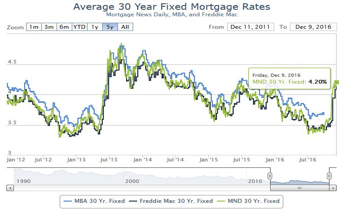

Apart from the above calculations, it is also beneficial for a borrowers to understand the trend in the mortgage rates over the last several years. Higher interest rates create higher lending costs for borrowers and reduce the total home value in the eligibility requirements. The chart example below shows the 30-year fixed mortgage rate (US):

SOURCE: PDX Listed Website, by Real Estate Agent Peter Park

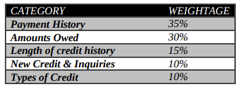

Establishing Credit Profiles

Before applying for a home loan, it is important for borrowers to assess credit score histories. The typical credit score is commonly called a FICO score, and this falls somewhere in a range between 330 and 830.

FICO calculates credit scores based on the following weightings:

Apart from these assessments, it is important for borrowers to start increasing reserves in savings accounts that will be used for emergencies and future loan settlements. This will help new homeowners make a more balanced decision in buying a dream home.